CRML executes Shareholder Agreement with Obeikan for JV

50/50 JV to build lithium refinery in Saudi Arabia

Exclusive offtake from Wolfsberg spodumene mine

US$0.03-0.04 cts/kWh power costs very attractive

BMW offtake agreement assigned to new JV – US$15m paid in

Lithium price in bottoming process

CRML pass through value still > A$0.50/ EUR share

KEY POINTS

JV execution allows renewed progress at Wolfsberg

Saudi Arabia lithium refinery will have very low energy and other operating costs

Lithium market may recover soon

Watch Gangfeng share price!

Acquisition of TANBREEZ rare earths will be a game changer for CRML

EUR still ridiculously priced

Re rating must come soon

Market cap A$78m on 1,398m shares @ A$0.054

Critical Metals Corp and the Obeikan Group have executed the Shareholders Agreement to form a joint venture with Critical Metals Corp to construct and commission a large-scale lithium hydroxide processing plant in the Kingdom of Saudi Arabia to process spodumene concentrate produced from the Wolfsberg Lithium Project located in Austria.

NASDAQ LISTING OF WOLFSBERG COULD BRING A$1.1BN TO EUR VALUE EUR is developing a portfolio of European lithium and rare earth projects that have considerable potential to significantly increase the market value of EUR and make it an early leader in European lithium production.

The key asset is the smaller scale 8.8ktpa LHM Wolfsberg Lithium spodumene mining project in Austria soon to be vended into CRML for listing on NASDAQ for US$750m in shares to EUR and lead to it becoming the first EU producer of battery grade lithium.

Exposure to exciting Victorian and Pilbara gold exploration

Kalamazoo (KZR) is a very interesting company with an impressive track record since listing less than four years ago. It has built an asset base and astutely secured funding that has placed the company in a strong position to confidently carry out its programmes over the next few years.

The company has its focus on two key areas, Victoria and the Pilbara, that are likely to be amongst the most important and exciting exploration centres in Australia for the next five years.

In Victoria, KZR has accumulated 100% ownership of three historic goldfields in the important 60moz Bendigo Zone that have a combined past production of over 8moz.

In the Pilbara, KZR’s projects include the recent Ashburton 1.6moz resource acquisition and those in the vicinity of DEG’s exciting Mallina Gold Project. KZR’s impressive growth has been through strategic asset accumulation and its future is developing them.

The potential of KZR’s tenements and its corporate character have been recognised by Quinton Hennigh, President of Novo Resources and adviser to Kirkland Lake on Fosterville and also KL.TSX Chairman Eric Sprott with respective shareholdings in KZR.

Call me to participate. Barry Dawes BSc F AusIMM MSAFAA Executive Chairman Martin Place Securities +61 2 9222 9111 bdawes@mpsecurities.com.au

LKE has a lithium development strategy with projects in the prime Argentinian brine producing regions and utilising innovative technologies to minimise operating costs and to maximise earnings and sustainability benefits.

LKE’s 4.4mt LCE Kachi resource will utilise Lilac Solutions ion exchange technology in its project with a PFS due shortly for 2023 production startup.

Lithium sector undergoing improved conditions as supply and demand match.

The rise and rise of the lithium-ion battery is changing the world.

The versatility of this technology for application from smartphones, domestic appliances, power storage to Electric Vehicles (hereon EVs) implies universal acceptance and dependence. The advent of the high tech chemical refiner and processor for battery plants is changing the lithium industry.

It becomes critical to understand that whilst lithium prices are soft it does appear that they are bottoming and as the near term market balance is being sorted out. Underlying battery demand is inexorably rising between 15-18% per year together with EV and energy storage demand and will eventually impact the lithium price.

LKE has globally significant resources and has Lilac Solutions’ innovative approach to lithium recovery from brines.

Ion exchange technology cuts out the time and capital intensive evaporative process from the flow sheet.

Developing Quality Gold Exploration Portfolio in WA

Torian has quality exploration tenements in two prolific gold production regions in Western Australia and is ready to resume activity after a period of tenement rationalisation and management changes.

Kalgoorlie Region tenements have six projects including the Zuleika Shear, Credo Well, Mt Monger and Gibraltar. This Kalgoorlie region has a widespread blanket of transported cover and little outcrop and is undergoing a major re-evaluation and re-interpretation from basic principles as new gold hosting environments in the Black Flag Group (including sediments) are recognised. Over 127 targets have been identified by TNR on its tenements using geological and geophysical tools.

Leonora Region tenements have three projects Mt Stirling, Mt Stirling Well and Diorite. Mt Stirling is adjacent to RED.ASX’s very encouraging King of the Hills development and likely to provide near term cashflow from small scale mining.

Torian has accelerated the activity over its portfolio by farm-outs and is seeking to achieve gold production and build cash by end 2020.

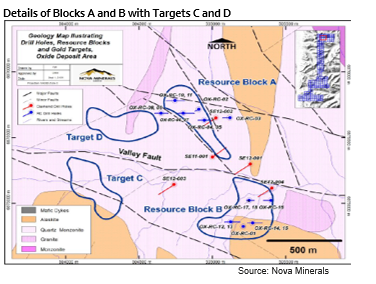

Nova Minerals (NVA) has the Estelle Gold Camp in the premier Tintina Gold Belt that hosts >220Moz in mostly bulk tonnage but high margin deposits.

Estelle has established a 2.5Moz JORC resource on Korbel Blocks A&B and the 2020 program is targeting a further 2-5Moz from here and in Targets C&D.

Officer Hill Gold Project with Newmont showing encouraging results chasing Callie-style mineralisation in the Tanami Region gold system.

NVA is fortunate in having a number of existing new or project mines in the Tintina Gold Belt for comparison so indications on capital and operating costs are current or recent.

Disclaimer: This commissioned report has been written by Martin Place Securities Pty Ltd. Data has been sourced from available public information and reflects the author’s own assessments.

Martin Place Securities has produced a commissioned research report on Torian Resources, a small company operating in and around Kalgoorlie with particular focus on tenements along the Zuleika Corridor about 40km west of Kalgoorlie. What began as an interesting region for a small cap exploration play for MPS clients, the Zuleika Shear west of Kalgoorlie (now considered in some circles to be the Zuleika Corridor) has turned out to be something far more significant for the Australian gold industry and for the major companies in this area:- Northern Star, Evolution, Tribune and Rand Resources.

This Zuleika Corridor is now Australia's fifth largest goldfield, producing over 400,000ozpa, and is expected to rise as new mines from NST and EVN in particular are brought on stream.

The K2 and Strzleckie Structures carry narrow very high grade veins that support high grade and low cost mines that are currently very profitable and are amongst Australia's highest grade producers.

This production growth in a single goldfield mining camp is unprecedented in Australia my experience.

The growth in resources is also very substantial and the technical evidence from NST in particular is that the strong growth will continue.

Whilst most DawesPoints readers will be aware of the spectacular +750% performance of the ASX Gold Index from 2000 into 2011 like this:

They may not be aware that WA and the Kalgoorlie region in particular did not participate and in fact gold production fell 50% into 2008.

The gold production renaissance now underway and the exciting performance of the Zuleika Corridor makes for outstanding investment opportunities in the areas around Kalgoorlie.

Torian Resources is very well placed here and the Company's management which includes MD Matthew Sullivan, who also discovered important deposits in Kundana itself and also Kanowna Belle, has assembled a tenement package that covers about 25% of the line of strike of the highly productive K2 structure along the Zuleika Shear.

Torian's tenements along the Zuleika Shear are well chosen and even the tenements in the NE beyond Mt Pleasant may prove up to be a pleasant surprise.

The company is small but the opportunity has large potential and is deserving of a thorough assessment.

The data indicates that the region is still substantially underexplored with <5% of drill holes to date exceeding 100m below surface.

Barry DawesBSc FAusIMM MSAA

I own TNR, NST, EVN, TBR and Cascade.

[button id="" css_class="" button_text="Download Torian Report" button_url="http://paradigmsecurities.com.au/wp-content/uploads/Torian_Resources_Ltd_Research_Report_Initiating_Coverage_.01.pdf" button_style="style-1"]

The gold price is beginning to show encouraging signs of beginning the next stage of the long term bull market that will take it to new highs over US$2000/oz.

The demand for gold from India and China already exceeds global mine production and is adding to high investment interest from Europe and North America. Central banks are also now significant net buyers so the overall gold market is tightening up. We also have to ask `who will be the sellers?’ to meet this demand at today’s prices.

Gold has already been rising in most currencies and the recent weakness in the A$ has pushed up the gold price up above A$1500/oz.

The ASX Gold Index has responded to the better gold market and is up 60% from its low in November but it is still 69% below the 2011 high when gold was only about A$1400/oz compared to A$1550 today. There is much to catch up.

Some Paradigm gold stock recommendations from the2014 December Dawes Points are up over 100% (NST +117, EVN115%) with others up over 50% (SAR +95%, MLX +83% and DRM +78%). The recent strong earnings reports from many of these companies and some with increased dividends can only get better in 2015 with a gold price A$150/oz higher.

Blackham Resources is one company that has outstanding prospects from its Wiluna gold mining project that Paradigm considers will provide outstanding short and long term returns as the entire Wiluna Goldfield is revived. With 4.7moz resources and a 1.3mtpa processing plant the project should have a long term future at gold production rates of over 100,000ozpa generating revenues of over A$150mpa.

Most Paradigm account clients hold BLK and should do very well as long term investors.

Risked milestones are provided to indicate an 18 month share price base target of A$0.90/share with potential of $1.57.

If you don’t have BLK and don’t have account with Paradigm you might be missing out!

Key Points

Engineering studies on mines and mill well advanced

Target of >80kozpa by mid 2016 then >100kozpa

Mill refurbishment capital costs set at <A$16m

Mine development costs estimated at <A$10m

Total funding requirement is estimated at <A$26m

Cash flow positive five months after major funding drawdown

Initial resources base in excess of 4.7moz and growing

Additional potential of up to 3moz in near mine exploration

Summary

Blackham Resources’ 1.3mtpa Matilda Gold Project to produce 100-110,000ozpa is coming closer to fruition with progress made on the mill rehabilitation process and the finalising of ore sources from the current 4.7moz resource. Exploration appraisals are also providing potentially significant new resources.

Higher A$ gold prices and the fall in the cost of mining contractor equipment and fuel costs should give this project even more attractive margins.

Paradigm has determined a Base Case Project NPV8at A$1,500/oz of A$173m (A$0.90 /share fully diluted) and a Standard Case Project NP V8 at A$1,500/oz ofA$303m (A$1.57 /share fully diluted). Risked milestones are provided to indicate an 18 month share price base target of A$0.90/share with potential of $1.57.

The growth in resources is also very substantial and the technical evidence from NST in particular is that the strong growth will continue.

The growth in resources is also very substantial and the technical evidence from NST in particular is that the strong growth will continue.